Trading Puts on Facebook

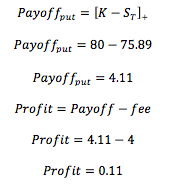

FB's current stock price is $75.89. A broker's market for the put option on the $80 strike expiring in 2 days is $3.75 bid at $4.00. Assuming no execution risk, what trade do you want to execute?

Assume that the risk-free interest rate is 0%, FB does not issue dividends, and that there are no transaction costs.

This section requires Javascript.

You are seeing this because something didn't load right. We suggest you, (a) try

refreshing the page, (b) enabling javascript if it is disabled on your browser and,

finally, (c)

loading the

non-javascript version of this page

. We're sorry about the hassle.

In this moment the put option is ITM, so its intrinsic value its positive and covers the fee of entering in to the contract, so we will take some profit.